Stalled ACA Reforms, Soaring Premiums, and the Human Cost in America’s Election Year

I. Introduction: The Persistent Healthcare Divide

The Affordable Care Act (ACA) reshaped the American healthcare landscape by expanding coverage, standardizing benefits, and strengthening consumer protections. At the same time, it entrenched deep partisan divisions that have persisted for more than a decade. Supporters view the ACA as a necessary foundation for equitable access to care, while critics frame it as an example of federal overreach that distorts markets. These competing narratives have defined healthcare politics since the law’s passage. Yet beyond ideology, the ACA’s mixed legacy reveals unresolved structural weaknesses. The divide today is less about whether the law exists and more about whether it delivers affordability.

Despite significant coverage gains, rising healthcare costs continue to undermine the ACA’s promise. Premiums, deductibles, and out-of-pocket expenses have increased faster than wages for many households. Insurance coverage no longer guarantees access to timely or affordable care. Many Americans remain functionally underinsured, exposed to financial shock in the event of illness or injury. These pressures are particularly acute in rural areas and among middle-income families who earn too much for assistance but too little to absorb high costs. The gap between coverage and care has widened.

As enhanced ACA subsidies expire and partisan gridlock blocks legislative fixes, millions face renewed financial vulnerability. Families confronting medical emergencies increasingly turn to debt, delayed treatment, or public fundraising to survive. Against this backdrop, President Trump’s proposal to provide direct healthcare payments to individuals has gained political traction. The idea reflects frustration with insurers and intermediaries, but its practical impact remains uncertain. In an election year, healthcare policy has become both a political weapon and a human crisis. The consequences of inaction are no longer abstract.

II. Stalled Promises: The Unfulfilled Vow to Repeal and Replace Obamacare

Republican opposition to the Affordable Care Act has been a defining feature of national politics since 2010. During President Trump’s first term, repeal and replace efforts dominated legislative priorities. Multiple bills were introduced, debated, and ultimately failed, most notably in 2017. While regulatory changes weakened certain provisions, the law itself survived intact. The failure to replace the ACA left a policy vacuum rather than a resolved alternative. Opposition succeeded rhetorically but not structurally.

The 2024 campaign revived promises to finally dismantle “Obamacare”. Candidates pledged a better system that would lower costs, expand choice, and preserve protections for preexisting conditions. Yet once again, no comprehensive replacement plan emerged. Public messaging emphasized flexibility and innovation without legislative specificity. Voters were offered broad assurances rather than policy detail. The pattern mirrored earlier repeal efforts that prioritized messaging over design.

By 2026, references to “concepts of a plan” have become emblematic of healthcare paralysis. Internal party divisions and narrow congressional margins have complicated consensus building. Policymakers have struggled to reconcile ideological goals with operational realities. Healthcare reform remains trapped between ambition and execution. As a result, the existing system persists without meaningful improvement. Americans continue to navigate a flawed status quo.

III. Expiring Subsidies: The Shockwave of Skyrocketing Premiums

Enhanced premium tax credits introduced under the American Rescue Plan and extended through the Inflation Reduction Act played a critical stabilizing role in the ACA marketplace. These subsidies reduced premium costs and expanded eligibility to millions of middle-income households. For many families, coverage became affordable for the first time. The policy helped sustain enrollment and limit churn. Its expiration at the end of 2025 marked a significant inflection point. The safety net weakened abruptly.

In 2026, enrollees began facing steep premium increases as enhanced subsidies disappeared. Estimates indicate that premiums for some households more than doubled. Middle-income families were particularly affected, as many lost eligibility for assistance altogether. Faced with higher monthly costs, millions risked dropping coverage. The coverage gains achieved over the past decade are now under threat. Affordability has once again become a barrier to enrollment.

The broader economic consequences extend well beyond individual households. Rising uninsured rates increase uncompensated care costs for hospitals and clinics. Safety-net providers, already operating on thin margins, face renewed financial strain. Delayed care contributes to worse health outcomes and higher long-term costs. Public health systems absorb the downstream effects of coverage loss. The expiration of subsidies reverberates across the healthcare ecosystem.

IV. Partisan Battles: Gridlock Over Fixes in an Election Year

Democrats have pushed to extend or permanently codify enhanced ACA subsidies. They argue that stabilizing premiums is essential to protecting coverage and economic security. Republicans, by contrast, emphasize deregulation and market-based solutions. These positions reflect fundamentally different views of government’s role in healthcare. Neither side has secured sufficient leverage to impose its vision. Legislative stalemate has become the default outcome.

The dynamics of an election year have further intensified gridlock. Razor-thin congressional majorities magnify procedural obstacles and partisan incentives. Healthcare has reemerged as a top voter concern amid rising costs. Both parties fear political backlash from compromise. Policy debates are shaped as much by electoral strategy as by substance. As a result, negotiations remain frozen.

Election-year posturing has delayed concrete action. Short-term extensions are debated while long-term reforms remain elusive. Families confronting immediate premium hikes receive little certainty. Uncertainty itself has become a defining feature of healthcare policy. Households are forced to plan without reliable information. The cost of delay is borne by patients, not politicians.

V. The Social Media Cry for Help: Crowdfunding and Insurance Battles

As formal safety nets weaken, Americans increasingly turn to social media for financial support. Platforms such as GoFundMe and Tik Tok have become informal mechanisms for paying medical bills. Campaigns seek assistance for surgeries, cancer treatments, and transplants. Many raise only a fraction of the required funds. Their prevalence reflects desperation rather than preference. Healthcare has become a public appeal.

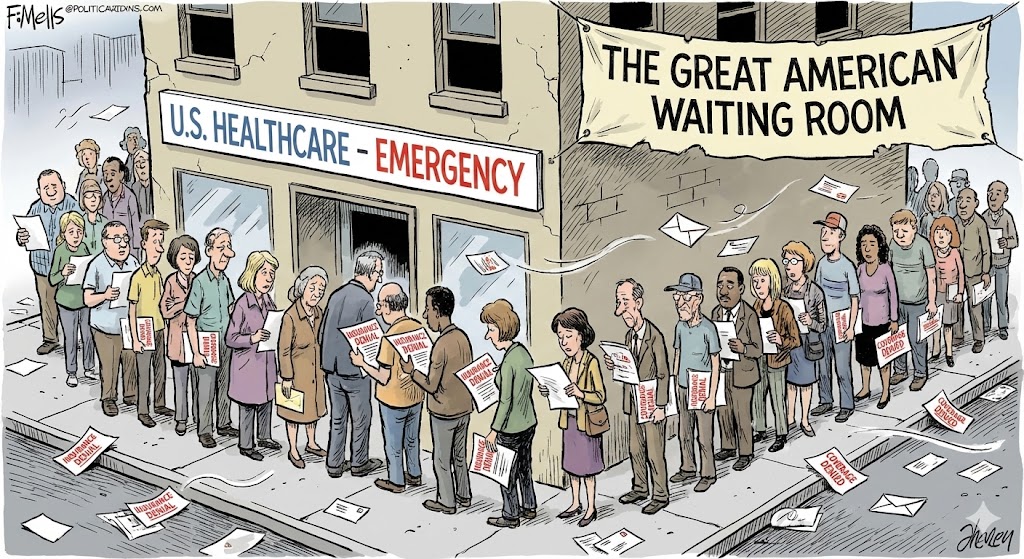

Insurance denials often drive these campaigns. Families report months of appeals, documentation requests, and phone advocacy. In some cases, public attention prompts insurers to reverse decisions. The process is emotionally exhausting and unpredictable. Approval can depend on persistence rather than medical necessity. Access to care becomes contingent on visibility.

The human toll is significant. Patients delay or abandon treatment while navigating administrative barriers. Loved ones are forced into roles as advocates and fundraisers. Social media exposes systemic failures while offering temporary relief. Community support fills gaps left by policy. The trend underscores the erosion of institutional trust.

VI. Trump’s Direct Payment Proposal: Innovative Relief or Financial Shortfall?

President Trump’s “Great Healthcare Plan” proposes shifting government assistance directly to individuals. Payments would be deposited into health savings style accounts rather than routed through insurers. Supporters argue this approach empowers consumers and bypasses bureaucracy. The proposal aligns with broader critiques of intermediaries. Politically, it resonates with voters frustrated by complexity. Substantively, it raises unresolved questions.

The plan also aims to lower drug prices and increase transparency. Direct payments are framed as a mechanism to encourage competition and consumer choice. However, details regarding funding levels, eligibility, and adjustment for income or health status remain unclear. It is uncertain whether payments would keep pace with rising costs. The absence of specificity complicates evaluation. Policy design remains incomplete.

Critics warn that fixed payments could expose patients to greater financial risk. High-need individuals may face significant out-of-pocket expenses. Low-income households could be underprotected if payments fail to scale adequately. Without regulation, disparities may widen rather than narrow. Innovation alone does not guarantee equity. The proposal’s impact depends on implementation.

VII. Corporate Interests and the Role of Middlemen

Pharmacy benefit managers and insurers occupy powerful positions within the healthcare system. Their pricing practices often obscure true costs from consumers. Critics argue that these intermediaries profit from complexity and opacity. Reform efforts threaten established revenue models. Industry resistance has been substantial. Structural change remains difficult.

President Trump has targeted middlemen as drivers of inflated prices. Proposals to eliminate kickbacks and increase transparency seek to disrupt existing incentives. Such measures could realign pricing structures and reduce costs. However, entrenched interests wield significant political influence. Regulatory change faces legal and institutional barriers. Momentum has been limited.

Consolidation across the healthcare sector exacerbates inequality. Mergers reduce competition and concentrate market power. Patients face fewer choices and higher prices. Corporate interests shape policy outcomes behind closed doors. The status quo persists at public expense. Accountability remains elusive.

VIII. Economic and Social Implications: A Nation’s Health at Stake

Medical debt continues to drive financial distress across the United States. Insured households remain vulnerable to catastrophic expenses. Many delay or forgo care due to cost concerns. Medical bills contribute to bankruptcy and long-term instability. Health insecurity undermines economic mobility. The consequences extend beyond healthcare.

The burden is not evenly distributed. Low-income families face disproportionate exposure to cost shocks. Rural communities encounter limited provider options and higher premiums. Minority populations experience compounded barriers to access and quality care. Structural inequities are reinforced by policy gaps. Health outcomes reflect these disparities.

Public trust in government solutions has eroded. Repeated promises have yielded limited relief. Cynicism grows as crises persist without resolution. Confidence in institutions declines alongside health indicators. The social contract appears increasingly fragile. Restoring trust requires action.

Thanks for reading The Brooks Brief Substack! This post is public so feel free to share it.

IX. Conclusion: Reimagining Healthcare Beyond Partisan Lines

Capitalism may excel as a system for business, but it has inherent limitations in healthcare. When profit motives guide medical decisions, patients can be denied care or charged exorbitant amounts for necessary treatment. Health insurance companies, rather than doctors, often determine who receives lifesaving procedures, creating perverse incentives that prioritize revenue over patient outcomes. Consolidation and market concentration amplify these effects, leaving vulnerable populations at the mercy of corporate interests. Pricing structures obscure true costs and reduce transparency, undermining trust and access. In a sector where timely care can mean the difference between life and death, the logic of profit conflicts with the moral imperative of medicine. A sustainable system must balance financial viability with human need to prevent preventable suffering and death en masse.

The American healthcare system stands at a critical juncture. Stabilizing coverage and controlling costs require bipartisan commitment. Incremental fixes are no longer sufficient. Policy must align with lived experience. Delay carries measurable human consequences. The stakes are high because citizens have already succumbed to this inefficient healthcare system.

Voters, advocates, and innovators have a role in shaping outcomes. Public pressure can elevate healthcare beyond partisan theater. Evidence-based solutions must replace rhetorical cycles. Transparency and accountability are essential. Sustainable reform demands political courage.

Without bold and equitable change, the system risks further fragmentation. Election promises may continue to echo without substance. The cost of inaction will be measured in lives and livelihoods that have changed for the worse. Healthcare cannot remain a bargaining chip. The nation’s health depends on it.