How Decades of Policy Failures Created a National Emergency

In January 2026, the American Dream of homeownership or even stable, affordable renting is increasingly out of reach for millions. Data from Harvard’s Joint Center for Housing Studies and the National Low Income Housing Coalition show renter cost burdens at record levels, with roughly half of all renters, more than 22 million households, spending over 30 percent of their income on housing. Millions more face severe cost burdens, devoting over half of their income to rent and utilities. The country also suffers from a shortage of at least 7.1 million affordable and available rental homes for extremely low-income households. This leaves only 35 affordable units for every 100 households that need them. At the same time, home prices remain near historic highs relative to wages. The income required to afford a median-priced home now far exceeds what typical families earn.

These conditions are often framed as the unavoidable result of supply and demand or post pandemic volatility. That framing obscures the reality that the crisis is largely man made. Decades of policy decisions have constrained supply, encouraged speculation, and failed to protect renters and first time buyers. Housing has been treated primarily as an investment vehicle rather than essential infrastructure. As a result, affordability has deteriorated even during periods of strong construction. The disconnect between policy intent and lived outcomes has widened. What was once a pathway to stability has become a source of uncertainty.

Purely market based solutions have repeatedly fallen short because housing does not function like other commodities. Developers rationally pursue the highest returns, which usually means luxury units rather than workforce or low income housing. Regulatory barriers and financing structures further skew production away from need. Low income households are left competing for a shrinking pool of aging units. When shortages persist, prices rise regardless of broader economic conditions. Without corrective policy, the market reproduces scarcity rather than resolving it.

Thanks for reading The Brooks Brief Substack! Subscribe for free to receive new posts and support my work.

The Zoning Straitjacket: How Local Rules Block Homes

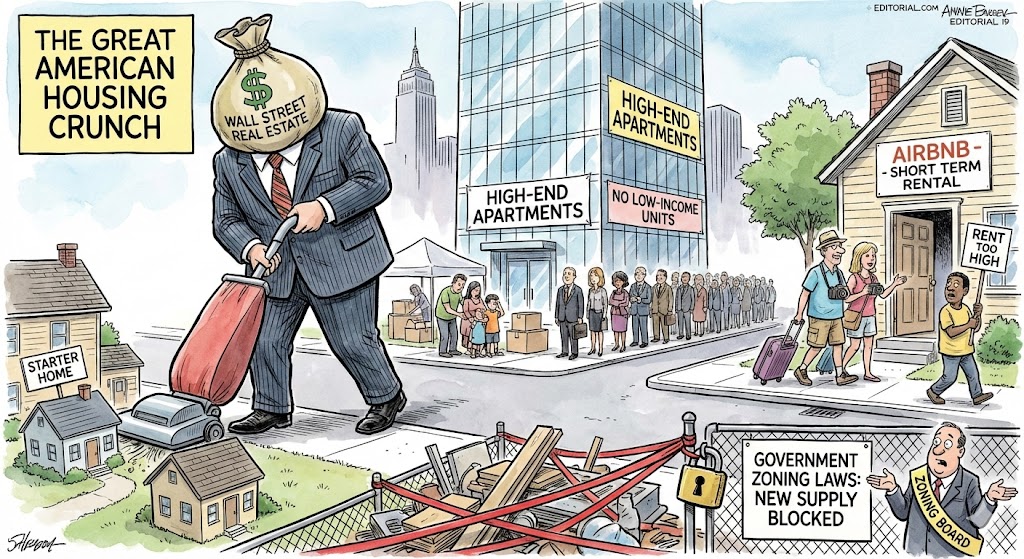

At the core of the housing shortage is the dominance of single family zoning across much of the United States. Rooted in early twentieth century land use rules and reinforced by decisions such as Euclid v. Ambler Realty in 1926, these policies prohibit apartments, duplexes, and townhomes on vast areas of residential land. In many cities, 70 percent or more of residential land is reserved exclusively for detached single family homes. This dramatically limits the number of homes that can be built in high opportunity areas. Over time, these constraints have hardened into political orthodoxy. The result is a chronic mismatch between where people want to live and what is legally allowed to be built.

The economic and social consequences are severe. Artificial scarcity pushes up rents and home prices while encouraging sprawl that increases transportation costs and environmental damage. Workers are forced farther from jobs, undermining productivity and quality of life. Restrictive zoning also entrenches racial and economic segregation by excluding lower income households from well resourced neighborhoods. Local control mechanisms amplify these effects by empowering small groups of residents to block new housing. Lengthy permitting processes, discretionary reviews, and lawsuits turn even modest projects into multi year battles.

Some progress has been made in recent years as states like California, Washington, Montana, and Texas moved to ease parking minimums, allow greater density, or reduce minimum lot sizes. These reforms represent an important shift in recognizing housing as a statewide concern rather than a purely local one. However, the scale and speed of change remain inadequate. Most reforms are incremental and leave core exclusionary structures intact. Even optimistic projections suggest it could take a decade or more for current policies to meaningfully close supply gaps. Without stronger state level preemption of local obstruction, shortages will persist.

Private Equity’s Takeover: Wall Street as Landlord

The modern wave of institutional ownership began in the aftermath of the 2008 financial crisis. Private equity firms such as Blackstone identified foreclosed and distressed homes as an opportunity for large scale acquisition. Hundreds of thousands of single family homes were purchased and converted into rental properties. Over time, these portfolios expanded and professionalized, creating a new asset class. Institutional investors now control roughly 3 to 4 percent of the national single family rental stock. While modest in aggregate, their presence is heavily concentrated in specific metro areas and starter home segments.

This concentration has tangible impacts on households and communities. Large landlords can impose rent increases, add fees, defer maintenance, and pursue aggressive eviction strategies with limited local accountability. Algorithmic rent setting tools have drawn scrutiny for potentially coordinating price increases across markets. By removing entry level homes from the for sale market, institutional buyers also reduce opportunities for first time homeowners. These dynamics disproportionately affect lower income families and communities of color. Housing insecurity becomes embedded in financial strategy.

Public policy has struggled to keep pace with these changes. Federal housing and finance programs often provide indirect support to large investors without requiring long term affordability or tenant protections. Recent political attention, including President Trump’s January 2026 proposal to restrict large institutional buyers from acquiring additional single family homes, reflects growing bipartisan concern. Yet symbolic measures are insufficient on their own. Effective reform would require limits on excessive concentration, stronger tenant rights, and incentives for long term stewardship. Without these guardrails, private equity will continue to treat housing primarily as a speculative asset.

Short-Term Rentals: Tourism’s Hidden Toll on Neighborhoods

Short term rental platforms such as Airbnb and Vrbo have transformed local housing markets over the past decade. Millions of listings now operate nationwide, representing an estimated 1 to 2 percent of total housing stock. Many of these units are entire homes used year round for commercial purposes rather than occasional home sharing. In popular tourist destinations, the share is often much higher. These conversions remove housing from the long term rental market. The financial incentive to cater to visitors frequently outweighs commitments to local residents.

Research shows that short term rentals can measurably increase nearby rents and home prices. Studies estimate that each additional listing may raise local rents by 0.4 to 3 percent, with similar effects on sale prices. While these impacts are highly localized, they are significant in already tight markets. Neighborhoods experience displacement as long term tenants are priced out. Local services suffer as communities hollow out. What appears as a tourism boom often masks a housing squeeze.

Municipal responses have varied widely. Some cities have implemented caps, bans, or principal residence requirements to curb commercial operations. Others have struggled with enforcement due to limited resources or platform resistance. In many cases, regulations arrived only after significant damage had been done. Short term rentals are not the sole driver of the national crisis, but they exacerbate shortages where demand is highest. Without consistent rules and enforcement, their negative effects will continue.

Why the Free Market Alone Cannot Fix This

Proponents of deregulation often argue that simply building more will resolve affordability concerns. While increasing supply is essential, the type and distribution of new housing matter greatly. Left to its own incentives, the market prioritizes high end units that deliver the greatest returns. Luxury apartments and condos dominate new construction even in cities with acute affordability crises. This pattern persists regardless of overall production levels. As a result, new supply often fails to reach those most in need.

Housing markets also exhibit classic market failures. Land is finite, development is slow, and information asymmetries disadvantage tenants and buyers. Scarcity premiums reward holding and speculation rather than broad access. In lower income segments, cost pressures can lead to disinvestment and deteriorating conditions. Wage stagnation and inequality further weaken the ability of households to absorb rising costs. These structural issues prevent self correction.

Government therefore has an indispensable role. Removing barriers is necessary but insufficient on its own. Public policy must actively shape outcomes through investment, regulation, and enforcement. Social housing models, nonprofit development, and long term affordability requirements can counterbalance market distortions. Without such intervention, affordability gains will remain elusive. The evidence from decades of experimentation is clear.

Thanks for reading The Brooks Brief Substack! This post is public so feel free to share it.

A Path Forward: Bold Reforms or Continued Crisis

America’s housing emergency reflects choices made over generations. Reversing course requires a comprehensive and coordinated strategy rather than isolated fixes. Zoning reform must move beyond pilot programs toward widespread liberalization. State governments should override exclusionary local rules and require meaningful density in high opportunity areas. Eliminating parking minimums and allowing multi family housing by right are critical steps. Supply must increase where demand is strongest.

Addressing speculation and consolidation is equally important. Policymakers should consider caps on institutional ownership in vulnerable markets and strengthen tenant protections nationwide. Transparency and limits around algorithmic rent setting deserve serious scrutiny. Tax policy can discourage short term speculation while rewarding long term affordability. These measures would help realign housing with its social function. Stability should be valued alongside efficiency.

Short term rentals and public investment also demand attention. Principal residence requirements and targeted caps can preserve housing in stressed neighborhoods. Revenues from tourism should support local affordability funds. At the federal level, expanded funding for affordable housing production, preservation, and vouchers is essential. Without sustained public commitment, reforms will fall short. In 2026, the question is not whether action is possible, but whether continued inaction is acceptable.

Leave a Reply